India is one of the fastest emerging economies in the world, but do you know how huge is India’s alcoholic beverage market is in terms of both consumption and fiscal impact?

After GST and Stamp duties, Excise Duties is the largest source of States’ Own Tax Revenue (SOTR), and a major part of State finances.

Annually, alcoholic excise collections are estimated at ₹2.5–3 lakh crore, and stays a most reliable revenue source. Excise duty tax provides 10-20 percent of the total tax revenue for many States and thus helps fund welfare programmes, infrastructure and public services.

India presents a paradox when it comes to alcoholic taxation. There are States, which heavily rely on Excise Duties,

For instance, Punjab gets nearly 20 percent of its total revenue from them. Kerala collects around 15 percent, due to high consumption and strong regulations, while other states collect much less.

Gujarat enforces prohibition and collects less than 5 percent from alcohol taxes, sacrificing revenue for social and cultural reasons. The differences highlight tensions between fiscal reliance and moral regulation.

This forces states to balance economic needs with public health and cultural values.

What makes states rely so heavily on the revenue from alcoholic beverages? One of the reasons is the economic nature of alcohol demand.

The consumption of alcohol is relatively price inelastic, meaning people don’t drastically reduce their drinking despite an increase in prices due to taxes.

Therefore, this creates a predictable revenue stream, unlike more volatile property taxes or stamp duties. As the national collection is approximately estimated at ₹2.5–3 lakh crore annually, alcohol excise duties provide states with a stable revenue stream, which states use to build infrastructure, fund welfare programmes, and provide public services.

Then, what is the problem or issue? Unfortunately, the revenue earned from alcohol taxation isn’t just about economics, but is also a socially sensitive issue.

Widespread alcohol consumption brings significant health and social challenges, while high taxes can lead to an increase in illicit liquor markets.

It is a tough balancing act for policymakers, as they need to ensure fiscal stability while addressing health concerns and preserving the social culture.

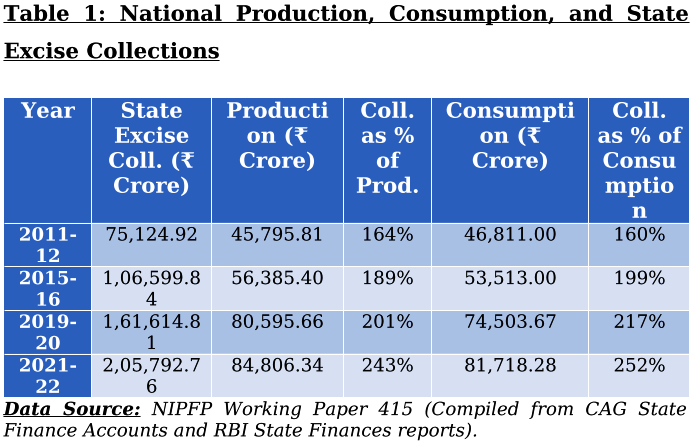

The Data – State Revenue Trends

Table 1 indicates that the State excise collections grew from ₹75,125 crore in 2011-12 to ₹2,05,793 crore in 2021-22. It has outpaced the growth in the formal production and consumption metrics (GVA/PFCE). The state tax collections increased by 174 percent (to be more precise 173.93 percent) during this period.

This divergence suggests aggressive tax mobilization strategies implemented by the states over the decade is successful, as the excise collections exceeded the recorded economic base figures.

The following table presents the macro-level trend of revenue generation from alcoholic beverages at current prices.

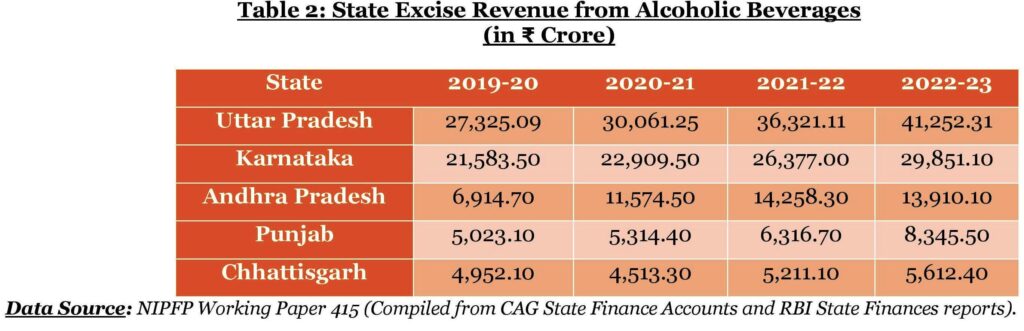

The above table shows a massive country-wide surge in tax collections. However, the actual implementation and revenue generation vary significantly from state to state.

This is due to unique, localized liquor distribution models. To examine these regional differences, Table 2 highlights specific alcohol revenue collections across five major states over the latest four-year period.

This table shows how alcohol revenue grew over the four-year period. Looking closely, it is clear that even during the 2020–21 pandemic, collections in major states like Uttar Pradesh and Karnataka continued to grow.

This growth happened because they restructured their pricing models. Meanwhile, states like Andhra Pradesh saw a quick revenue increase due to changes in state distribution policies.

As we look at the raw cash collections (Table 2), it shows how much money each state gets or brings in. However, it does not show how important that revenue is to the State.

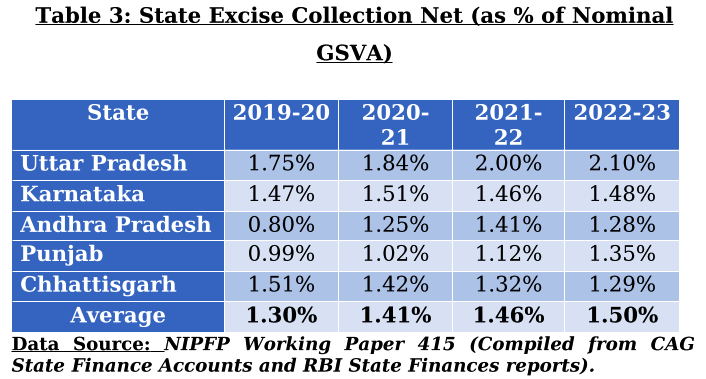

To understand this economic impact and revenue productivity, it is pertinent to look these collections as a percentage of the Gross State Value Added (GSVA). Table 3 provides this structural breakdown along with the five-state average over the same period.

This table clearly shows the increasing economic dependency of states on alcohol duties. In the past four year period, the average revenue share across these five states increased from 1.30 percent to 1.50 percent of their total nominal GSVA.

Interestingly, despite economic disruptions during the pandemic fiscal year 2020-21, the overall average increased to 1.41 percent, proving that alcohol remains a strong and indispensable economic anchor for state governments when other tax revenues shrank.

Uttar Pradesh tops the table and shows the most aggressive growth with its revenue share increasing to 2.10 percent in 2022-23. Even in the pandemic fiscal year (2020-21) its share as increased to 1.84 percent.

The Dry State Paradox – Balancing the Budget without Alcohol

From the above analysis, it is clear that the revenue generation from alcoholic beverages are highly reliable for these states, as it is increasing year on year. This brings an important question — What will happen when a state completely gives up this highly lucrative and stable revenue source?

The answer can be seen in “Dry States” like Bihar and Gujarat. These two states voluntarily sacrificed thousands of crores in alcohol excise to prioritize public health and social welfare.

These state governments are forced to find a tough alternative to balance their budgets without this massive financial cushion.

To fill the massive fiscal deficit, these state governments must implement stricter spending cuts or aggressively maximize other local revenue engines like property registration fees, fuel VAT, and central government financial transfers.

Conclusion

The future outlook of state fiscal health will depend entirely on how policymakers navigate this delicate tightrope between aggressive tax mobilization and crucial social policies.

However, states must find a sustainable solution to address these rising public health and social costs.

The long-term economic stability of Indian states lies in diversifying their local tax bases rather than depending on a social sensitive commodity.

Finding the right balance will determine whether a state can achieve true fiscal health without compromising the well-being of its citizens.