On 29 August 2025, the Ministry of Statistics and Programme Implementation (MoSPI) released a press note on the Quarterly Estimates of Gross Domestic Product (GDP) for the April-June Quarter (Q1) of Financial Year (FY) 2025-26, alongwith its expenditure components both at constant (2011-12) and current prices.

This article sees the sectoral and overall growth rate, sectoral analysis and implications of the results on the economy and ends with a conclusion.

Let’s get started.

Growth rate of Q1 of 2025-25

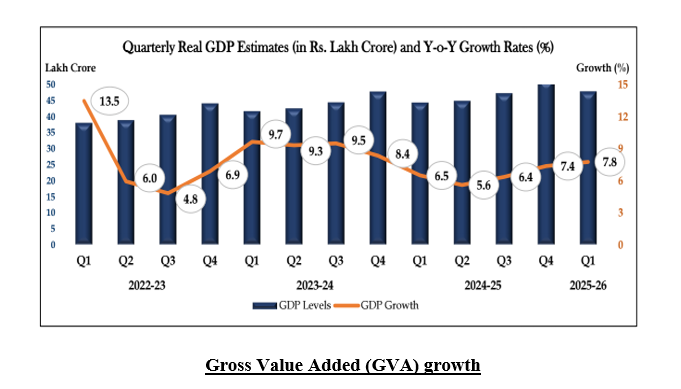

In the first quarter of FY2025–26, India’s economy showed impressive growth, achieving a solid 7.8 percent increase in real GDP, which was considerably better than what the market anticipated and surpassed the 6.5 percent growth from the first quarter of the previous year.

India’s rapid economic growth, despite obstacles such as high tariffs and global instability, confirms its position as the world’s fastest-growing major economy.

Before going further into the data, let us take a look at the major highlights of the Q1 GDP 2025-26 data.

Major highlights

Gross Domestic Product (GDP) growth

Real GDP growth:

The Real GDP growth is estimated at 7.8 percent Year-on-Year (YoY), at ₹47.89 lakh crore as against ₹ 44.42 lakh crore in Q1 of FY 2024-25.

Nominal GDP growth

The Nominal GDP is estimated at 8.8 percent YoY, at ₹86.05 lakh crore as against ₹79.08 lakh crore in Q1 of FY 2024-25.

Real Gross Value Added (GVA)

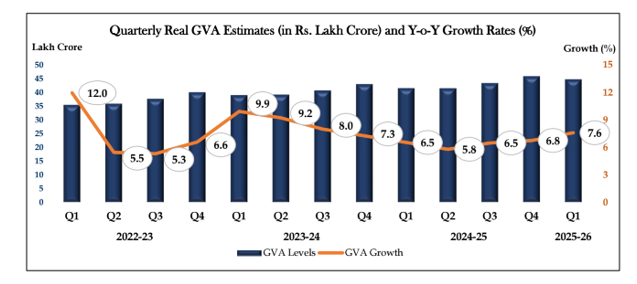

The Real GVA is forecasted to be ₹44.64 lakh crore during the first quarter (Q1) of fiscal year 2025-26, indicating a 7.6 percent growth from the ₹41.47 lakh crore of the Q1 of fiscal year 2024-25.

Nominal Gross Value Added (GVA)

It is estimated that the Nominal GVA for Q1 of FY2025-26 will be ₹78.25 lakh crore, which is an 8.8 percent growth from the ₹71.95 lakh crore recorded in Q1 of FY2024-25.

Strong sectoral performance

Sectors | Q1 2025-26 |

Agriculture | 3.7% |

Manufacturing | 7.7% |

Construction | 7.6% |

Services (Tertiary) | 9.3% |

Sectoral Analysis

- Agriculture and Allied Activities

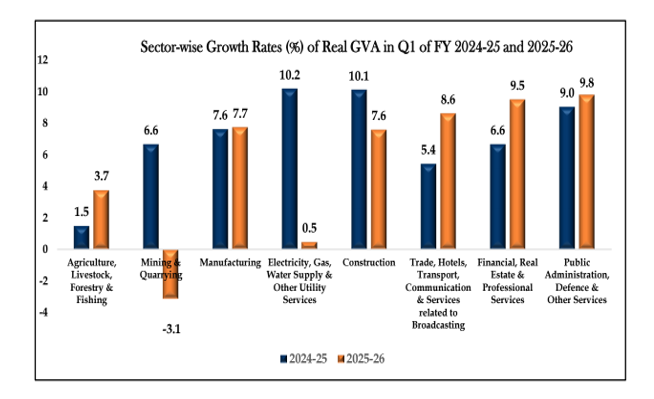

Agriculture grew by 3.7 percent, showing a remarkable increase from 1.5 percent Q1 of last year, supported by favourable monsoon conditions and strong Rabi and kharif crops sowing.

- Mining and Utilities

Mining contracted by 3.1 percent, largely due to flood-related disruptions. Utility services grew marginally at 0.5 percent, indicating subdued demand or supply constraints.

- Secondary Sector

Manufacturing and Construction both posted strong growth rates of 7.7 percent and 7.6 percent, respectively. These gains reflect increased industrial activity and infrastructure investments.

- Tertiary Sector (Services)

The services sector led the charge with a 9.3 percent growth, driven by robust expansion in financial services, real estate, and public administration. This marks a sharp rise from 6.8 percent in Q1 FY 2024–25.

Expenditure-Side Dynamics

Private Final Consumption Expenditure (PFCE)

PFCE grew by 7.0 percent, slightly lower than last year’s 8.3 percent, signifying cautious consumer sentiment.

Government Final Consumption Expenditure (GFCE)

GFCE increased by 9.7 percent, reflecting front-loaded fiscal spending.

Gross Fixed Capital Formation (GFCF)

GFCF rose by 7.8 percent, indicating healthy investment activity.

Sector-Wise GDP Growth Breakdown (Q1 FY 2025–26)

Sector | Growth Rate (YoY) | Key Insights |

Agriculture & Allied Activities | 3.7% | Strong rabi output and a favourable monsoon boosted farm income |

Manufacturing | 7.7% | Driven by auto, electronics, and FMCG production |

Construction | 7.6% | Infrastructure push and housing demand sustained momentum |

Electricity, Gas, Water Supply | 0.5% | Sluggish due to lower industrial demand and grid constraints |

Mining & Quarrying | –3.1% | Disrupted by floods and regulatory bottlenecks |

Trade, Hotels, Transport, Communication | 9.1% | Tourism rebound and e-commerce expansion led the way |

Financial, Real Estate & Professional Services | 9.4% | Credit growth, fintech adoption, and real estate boom |

Public Administration, Defence & Other Services | 9.2% | Higher government spending and welfare disbursements |

Important Implications

There are several important implications of the results of Q1 of FY 2025-26

- Agriculture is stabilising but remains vulnerable

Agriculture’s 3.7 percent increase is a positive development, especially considering the poor results from the previous year. However, the sector still heavily relies on the monsoon and is susceptible to climate shocks, highlighting the need for agri-tech adoption and irrigation reform.

- Manufacturing and Construction are holding strong

India’s industrial sector is gradually growing, with construction and manufacturing expanding at a rate of about 7.7 percent. This growth reflects the effectiveness of initiatives like PM Gati Shakti and Make in India, offering hope for job creation in rural and semi-urban areas.

- Mining and Utilities pose real concerns

Utilities saw minimal growth, while mining contracted by 3.1 percent, indicating potential underinvestment in energy infrastructure or supply chain bottlenecks. Policy focus is crucial in these sectors, especially as India aims for mineral self-reliance and energy security.

- Services are evolving to drive India’s growth

The services sector’s growth of over 9 percent signals a shift towards a more urban, digital, and consumption-driven economy, particularly in finance, real estate, and public administration. This trend underscores the rising demand for digital infrastructure, skilled labour, and urban housing, presenting opportunities for both domestic and international investors.

- Government expenditures are bolstering growth

Significant growth in capital formation and public administration suggests that fiscal policy is driving much of the economic progress. While this supports short-term growth, questions arise about long-term sustainability and the need to attract private investment.

- Global risks could disrupt momentum

External factors like U.S. tariffs and volatile oil prices pose risks that could impact future quarters despite India’s strong domestic performance. Maintaining macroeconomic stability, boosting local demand, and diversifying exports will be critical for India’s resilience.

Conclusion

In summary, these growth rates demonstrate resilience with some limitations. India is experiencing rapid expansion, but moving forward requires smart policy decisions, fair growth strategies, and strategic investments.