New Delhi: A worrying trend in household debt composition has been brought to light by the Reserve Bank of India’s (RBI) most recent financial stability report: An increasing proportion of borrowings are being used for consumption rather than asset building.

Funding consumption, not investment

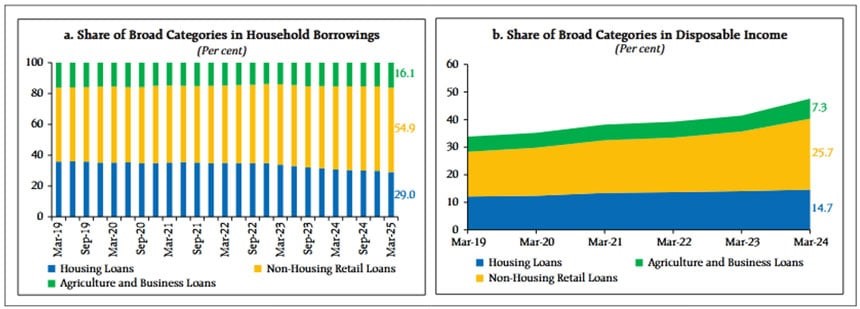

In India, non-housing retail loans, which are mostly used for consumption, currently account for around 55 percent of all family debt.

As of December 2024, India’s GDP comprised 41.9 percent household debt.

The RBI is concerned about the increasing use of credit for consumption, even though it’s lower than in other emerging market economies. The ready availability of personal loans increases the risk of financial difficulties and accumulating unmanageable debt.

According to the RBI report, the non-housing retail credit, including personal loans like credit card dues and consumer durable financing, now accounts for 25.7 percent of households’ disposable income as of March 2024. In terms of growth, this category has continuously exceeded commercial, housing, and agricultural loans in recent years.

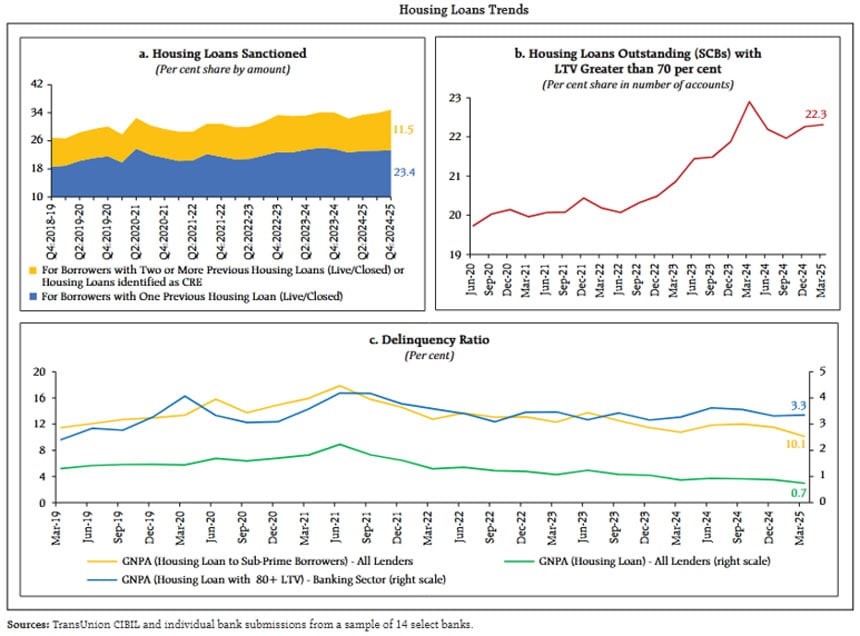

The gross-non performing asset ratio (GNPA) of housing loan was 3.3 percent as of March, while GNPA for housing loans to sub-prime borrowers stood at 10.1 percent.

As of March, the gross non-performing asset ratio (GNPA) for housing loans was 3.3 percent, and the GNPA for sub-prime borrowers was 10.1 percent.

In contrast, housing loans only comprise 29 percent of overall household debt, with growth mainly driven by existing borrowers availing top-up or additional home loans. This changing debt landscape poses challenges for financial stability in the country.

According to RBI data, a growing percentage of home loans have loan-to-value ratios higher than 70 percent, which suggests increased indebtedness. Although they still have higher delinquency rates, these borrowers have shown a considerable decline during the Covid-19 era.

With per capita debt increasing from Rs 3.9 lakh in March 2023 to Rs 4.8 lakh by March 2025, primarily as a result of higher-rated borrowers, India’s household financial balance sheets appear to be durable.

The financial worth of households increased significantly in FY23–24, according to the central bank.

“Deposits and insurance and pension funds formed nearly 70 per cent of household financial wealth as of end-March 2024, even as the share of equities and investment funds has increased,” says the RBI report.

The RBI noted that the percentage of prime and above-rated clients has increased in terms of both the number of borrowers and the total amount of outstanding loans, which is positive for overall debt serviceability and financial stability.

Despite the economy’s general stability, the RBI emphasised the significance of keeping an eye on debt accumulation trends, particularly among lower-rated and highly leveraged families.

Although it is anticipated that monetary policy easing will lessen repayment obligations, the central bank issued a warning about possible systemic risks due to the consistent rise in consumption-led borrowing.

According to the RBI’s assessment, household lending risks to the financial system are currently under control. However, it stressed the importance of keeping a close eye on the changing debt landscape, which is becoming more and more focused on consumption, in order to avoid vulnerabilities in the future.

Conclusion

Household lending risks to the financial system are currently under control, but there is concern that a significant portion of loans are being used for consumption rather than investment. This trend can be attributed to two main factors: cheap loans and a shift in consumption patterns.

Consumers are now able to access consumption loans with zero percent interest rates, leading to a change in their spending habits. Even for everyday purchases, such as a basic phone, individuals are opting to use these loans, and in some cases, even for more expensive items.

This shift in behaviour is altering the traditional saving and investing culture that were once prevalent in the Indian economy.